zurch1818

-

Posts

677 -

Joined

-

Last visited

Content Type

Profiles

Forums

Blogs

Events

News

2026 Milwaukee Brewers Top Prospects Ranking

Milwaukee Brewers Videos

2022 Milwaukee Brewers Draft Picks

Milwaukee Brewers Free Agent & Trade Rumors, Notes, & Tidbits

Guides & Resources

2023 Milwaukee Brewers Draft Picks

2024 Milwaukee Brewers Draft Picks

The Milwaukee Brewers Players Project

2025 Milwaukee Brewers Draft Pick Tracker

2026 Milwaukee Brewers Draft Pick Tracker

Store

Downloads

Gallery

Everything posted by zurch1818

-

Those watermelons are bullpen pieces.

-

Thanks for the suggestion, Homer. After hearing your advice, I messaged the hospital the following day and they got back to me a few hours later. I had a good conversation with their representative. I didn't get an explanation of why it exactly happened but he did say he was going to bring my complaint up in their next staff meeting and he was deeply sorry about it. It would have been nice to have the doctor personally message me instead of the rep who always has to wear that hat. I just hope my complaint helped save someone from getting addicted. Opioids are not something to mess around with (unless they are absolutely necessary).

-

Didn't the S&P go up by 24% in 2023? I know a lot of my growth mutual funds are up by more than this percentage but I don't really care enough right now to look at the exact numbers. Maybe you started investing later in the year? Or maybe you beat the market by 10.55%? I'm just trying to understand.

-

Hospitals pushing opioids on me today. On the 23rd, I burned myself pretty badly. The story is right up there with Matt Wise's salad tongs and Lucroy's suitcase (not important unless someone is dying to know the story...I can even post some pictures in a spoiler if you really want to see it). Anyway, I did some telehealth visits given the holiday timing and I got a doctor's recommendation and prescription ointment to put on the burns. That 24/7 urgent care anywhere system I'm actually very happy with. Anyway, it's now about 5 days since it happened and I figured I would get it looked at by the UW just to make sure everything is healing as it should and to check one spot I wasn't sure if it was second degree or third degree. I went into urgent care and they referred me to the burn team with the ER (which I was fine with). At the ER, the general ER doc and also the burn doc just kept pushing opioids at me for pain...even after I said my pain was a 0 when stationary and 1 to 3 when I bent the wrong way or had to reach to tie my shoe. It even got to the point where I finally agreed to take ibuprofen and Tylenol (first meds I've taken for pain) since they were going to clean the wounds with soap and water. After my consult with the burn doc, a nurse stopped by with medication. She scanned my bracelet, it showed up as being rejected, and she was very confused. She then came back with ibuprofen and Tylenol. It was oxycodone in the first order...not what I was expecting or agreed to. She said they cancelled the order after she picked it up. Why was that order even put in when I said I didn't want it? Is that just standard protocol for burns? When getting discharged, the ER doc gave me a prescription for oxycodone and the overdose spray that I will not pick up. I'm happy with the care I got but I don't know what I would have done to get home and left our only vehicle at the ER given today's weather.

-

Yes. In all seriousness, I had to look back at the '05-'06 team (my freshman year of college at UW). I completely forgot that the Bradley Center hosted the championship. I also went down the line of players...Elliott, Pavelski, Earl, Skille (very hyped for what his career was), Street, Dowell, Gilbert, among others. I also saw Ryan Jeffrey, whose wallet I found on the street. My roommate went to HS with him, so it was easy to return. I believe he called him with his brand new RAZR phone. Wow, am I starting to sound like my dad reminiscing about an old sports team.

-

YouTube's algorithm wanted me to watch this on the history of the first NHL season, so I did...and there weren't 6 teams, which got me very confused. Additionally, there were teams I've never heard of in the original league. Then I found this Kieth Olberman video to drive the point home. He's pretty entertaining. Disclaimer...the one thing it seems he didn't get quite right is the original team in Toronto was technically the Arenas, but the media dubbed them the Torontos.

-

I agree with this. There's always the jump shot free throw to help the mental aspect.

-

It's a male first name...just like Bill, Michael, etc. That's why it's so odd that there is a concentration of them on our cul de sac...because Randy isn't really that common of a name. My son might just think it is a male neighbor because they are all around us.

-

Very interesting reading on starter houses. Thanks for posting. One other anecdote to add (at least in the Madison area), a lot of the new houses are not starter-sized...but are built on starter-sized lots. You can basically jump into your neighbor's house from your house without touching the ground. Or better yet, as my dad says, you can see when your neighbor needs another beer. Don't get me started on current housing trend (putting white trim around everything to make it stand out). However when every house in a new neighborhood is a spec house stacked on top of each other, it overwhelms my brain with busyness. There isn't even room for trees. I bet the spec home market is not doing great right now with interest rates as high as they are. We struggled to find a house in our price range that was at least a half acre in size until we started looking for slightly older homes (ours was built in '94). It was remodeled to feel newer than it really is. However, it is nice having mature trees around us and neighbors not stacked on top of one another. We also live on a cul-de-sac without really any neighbors in our back yard, so my neighbor can't see my beer level. The only problem is we are the only house in our cul-de-sac that hasn't taken a tree out in our front yard. It's like we missed a memo. Complete side note, 3 of the 6 houses on the cul-de-sac are Randys (including both of my next door neighbors). I believe my son thinks a Randy is a male neighbor.

-

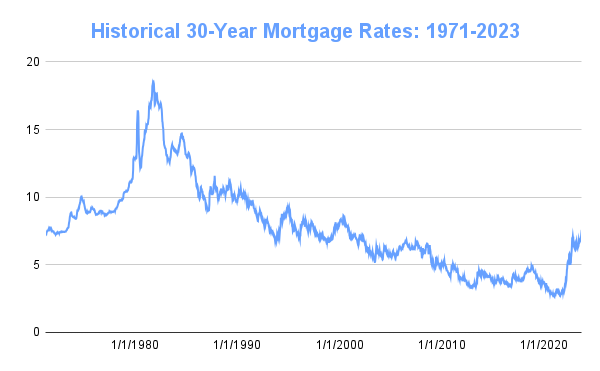

Good point. Here are the average 30 year mortgage rates over the last 50+ years. Interest rates are still historically pretty low...just way higher than what we are used to. I know there is a housing shortage...but I wish I understood why. Boomers should already have their houses and I don't believe the US population is exponentially growing at this time. Is it just families want bigger houses?

-

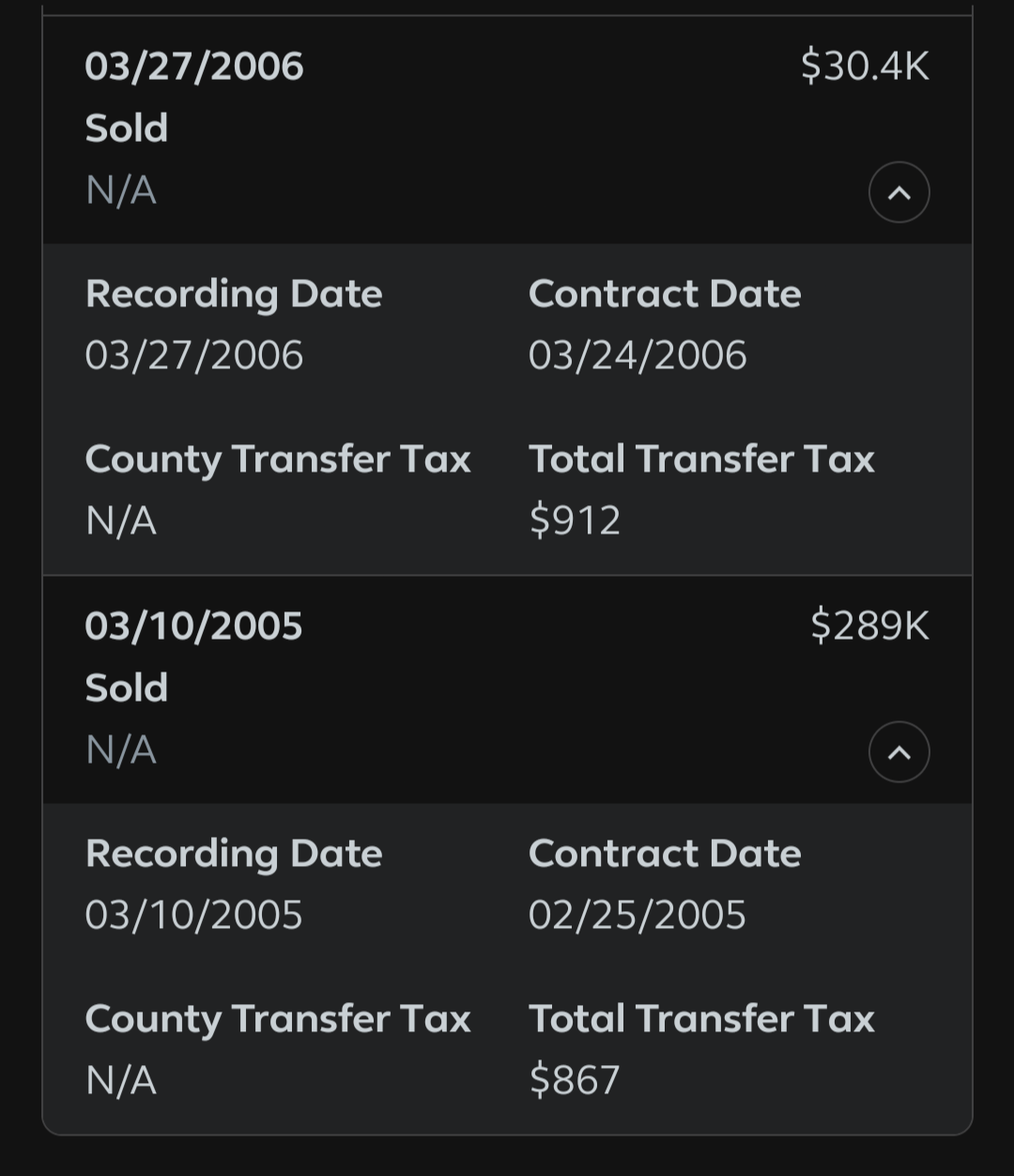

We actually just had the same thing happen to us. It wasn't the previous owners...but the one's before them, so 2005 at the latest. I ended up Googling them to see if I could find them, which it seems they were nearby. Then I used public property tax records to nearly confirm it, only 15 minutes away. I wrote the address on the envelope and put it back in the mailbox, as I didn't want to drive a half hour. Though it would have been interesting to just personally deliver the letter. The one thing I noticed in our public record is our house sold for twice within a year? And the second time was for about $30k. Can anyone with a real estate background provide a possible explanation? See below:

-

Amen. It sucks being up when you should be sleeping. I've been a zombie at work for longer than I can remember. Twin report: They have been sleeping 2 to 4 hours at a time for the last month in a half. It's crazy that when one of them is just crying uncontrollably, the other will just sleep right through it. It's also interesting that for them being identical, one of them is the one that gets up 75% of the time. The icing, I think their crying partially wakes our 2.5 year old to a point where he gets up 45 minutes after they are fed and get back asleep. My son will come into the twin's room (the room I'm sleeping in) and just starts talking because he "needs something" (but he doesn't know what when I ask him what) or is crying because he's terrified of thunder. Sometimes he will wake the babies and start the whole cycle over. We are working on whispering and staying in bed, but it's a long game. Having twins is difficult but barely doable. I don't know how people survive with 3+ babies.

-

None taken. You guys are simply more willing to be risky than me. I will say, if you get enough proceeds to pay off your primary residence in this sale, I'd recommend it. It's so nice from a cash flow perspective that a significant portion of my income isn't already spent. However, I'm guessing you will have a hefty tax bill doing so. LINK

-

Well it was only 400k in 2018 when we bought it. The Waunakee housing market is going bananas right now. Covid was the one time in recent history that it grew like the stock market. There is also a supply problem...especially when the interest rates were so low. I also saved money like crazy person from age 24 to 31. I lived super cheaply and when I got raises, I just saved more towards a house. I wasn't as aggressive with investing for retirement at that time. I bet it doesn't surprise you that I struggle to spend money and I get paralyzed doing it. Looking back, 2/22/22 was the payoff date and I'd do it all over again.

-

That sounds like a NPV question from my college days. The numbers don't seem that different from each other. Knowing the property will go up in value in 3 years...and not knowing what the rental cash flow is like makes it hard to answer. My guy says take the cash and run. Now if it were 50% more at year 3, that might change my opinion.

-

There's a risk factor that I just don't have to deal with. That's why I paid it off early. Now if I don't have a tenant or I lose my job, I don't have to worry about losing my house. Now my $1500 mortgage payment gave me an $18000 (since I was already paying taxes on it). I also don't have be a landlord to get this extra income and I don't have to pay interest (which I'm still not really seeing in your math). I'm not denying that I couldn't have made more money, but to take 3 steps forward and take 2 steps backwards on payments just wasn't worth the risk to me. It's not life changing money. Let me do the math. My roughly average 100k mortgage balance (round numbers average over the years) lost out on net 6% of gain over the time period (market rate - interest rate). That's 6k for 3.5 years...so about 20k. That's not life changing money. I just don't believe that borrowing huge amounts amounts of money is required to be wealthy...it's your income from your job that has a much larger ROI. I had money invested in a brokerage account until it was time to buy. I lived super cheaply and saved just about every bonus I got. Sure I was paying property taxes baked in, but I didn't pay a mortgage on top of it, so may rent payment was half of my mortgage + taxes. Renting long-term is not smart because the cost goes. A mortgage will lock in your price until you pay it off. I put 70% down which made paying it off quickly easier. Also, every year since buying my house, I've maxed out my Roth IRA, my wife's Roth IRA, and my Roth 401k before making extra payments...so I didn't completely lose out on investing. I'm 36 with a paid for house. Sure the house is half my net worth, but my investments should significantly outpace it in 10 years.

-

I had Phil Niekro for the Braves gold glove combo yesterday. Had to get a Milwaukee Braves reference in there. I'm waiting for the Cardinals Braves combo to put in Uecker. I wonder if he would count as a HOFer in immaculate grid?

-

Pixel phones have a built-in phone screening assistant for this. It detects if it is possible spam and if the assistant is not sure, Google will answer and give a transcript of what they are saying and also give you options of things to ask. I think Google's engineers did a fantastic job at creating this feature. It's also not a new feature as I've had it since 2018 (when I got my first Pixel phone).

-

Yes...I'm not going to deny that leveraging the value isn't a way to get more value out of it. You are also paying property taxes on the assessed value each year. My property taxes last year on my $500k house in a suburb of Madison were $8.5k, so the net gain in your 2% scenario for me (since my house is paid for) would only be $1.5k. Additionally, with how mortgages are set up, you pay the interest up front, so that also should get accounted for to in your scenario. On my mortgage that got paid off in under 3.5 years, I paid 20k in interest (roughly a third of the interest on the minimum payment amortization schedule). I feel like the lender's get a pretty sweet gig. They get this return with no property taxes or other expenses. Furthermore, that gain in value is now tied up into something you can't easily access unless you get another mortgage (HELOC) and pay more interest. I like being liquid. This is toobimportant to me. You could have instead invested that $70k you put down in the market and with the rule of 72, it will double in value every 7 years (assuming a a 10% interest rate). It will be worth roughly 230k after 12 years. But you have to pay cap gains on the gains, so total gain is (230 - 70)*(1-0.15) = 136k, not bad for only 12 years...but let's say you let it go 28 years (4 doubling periods). 70*2*2*2*2=1.12 million (890k net gain after cap gains). As Einstein says... The bottom line is, yes, I agree with you that what I said was not quite right, but the ROI isn't nearly as great when considering other expenses. This is why I said the increase is basically a few percentage points above inflation. You can make money on it no doubt, but it may not make you wealthy. Now paid for rental properties = cash flow!!! Especially if you know how to buy properties under market value. Also, diversifying assets between real estate and the market is also smart. There's also an aspect of real estate that takes time. It's something not required with stocks. Hopefully it won't come back to bite me.

-

Is there a way for you to retain ownership until they completely pay you? It's essentially what is happening. You can let them do the reno while still being the official owner. It's just if they default, you won't have to sue since you are still the property owner. I'm guessing your lawyer can come up with a way to make this happen in the contract.

-

First off...congrats on getting an offer you are considering accepting. That's not always easy. Let me preface this by saying that I'm not a real estate expert. I'm only speaking from my experience on paying off my house in 3.5 years. I also have no interest in ever owning rental property (though I could probably start this in a few years and buy my first property with cash...being a landlord is just too much work for me with having 3 kids under 3). I'd take the cash offer and here's why. If they are going to do significant work on it and they go under, you are going to be stuck with a house that may be difficult to sell as not many people are interested in buying a house halfway through a renovation (unless they get it at a good discounted price). Nope...it's just not worth the headache in my opinion. I don't want my money tied up in something I don't have control of...plus you may struggle to find renters to live in halfway renovated space. Stay liquid (that's the new water 😀). Real estate itself is actually not a great investment. It does help diversify your assets and isn't volatile, but only goes up in value a few percentage points above inflation (LINK). It only becomes lucrative when you have no payments and you can get rental income on top of the increase in value. I'm going to guess that the 6.75% interest payment is going to be way less than what your current rental income is at this. Sure 6.75% is a good interest rate, but when you consider that the S&P has gone up 17% this year, it doesn't look as great. Granted, not every year will do that, but on average, the yearly return of the S&P has been 10.5% over the last 100 years. The bottom line is the track record of the stock market will likely have a better rate of return (without the rental income). I'm not a bond expert either, but Louis's bond above gets more interest. Heck, we have a HYSA that is getting 4.25% now, which I know we can get more but it's not as convenient. It's an emergency fund. For the volume of money we are keeping in the account, it's only 100s of dollars different a year and the interest won't make us wealthy. That's a job for the brokerage bridge retirement account and Roth 401k/IRA accounts. Set it and forget it.

-

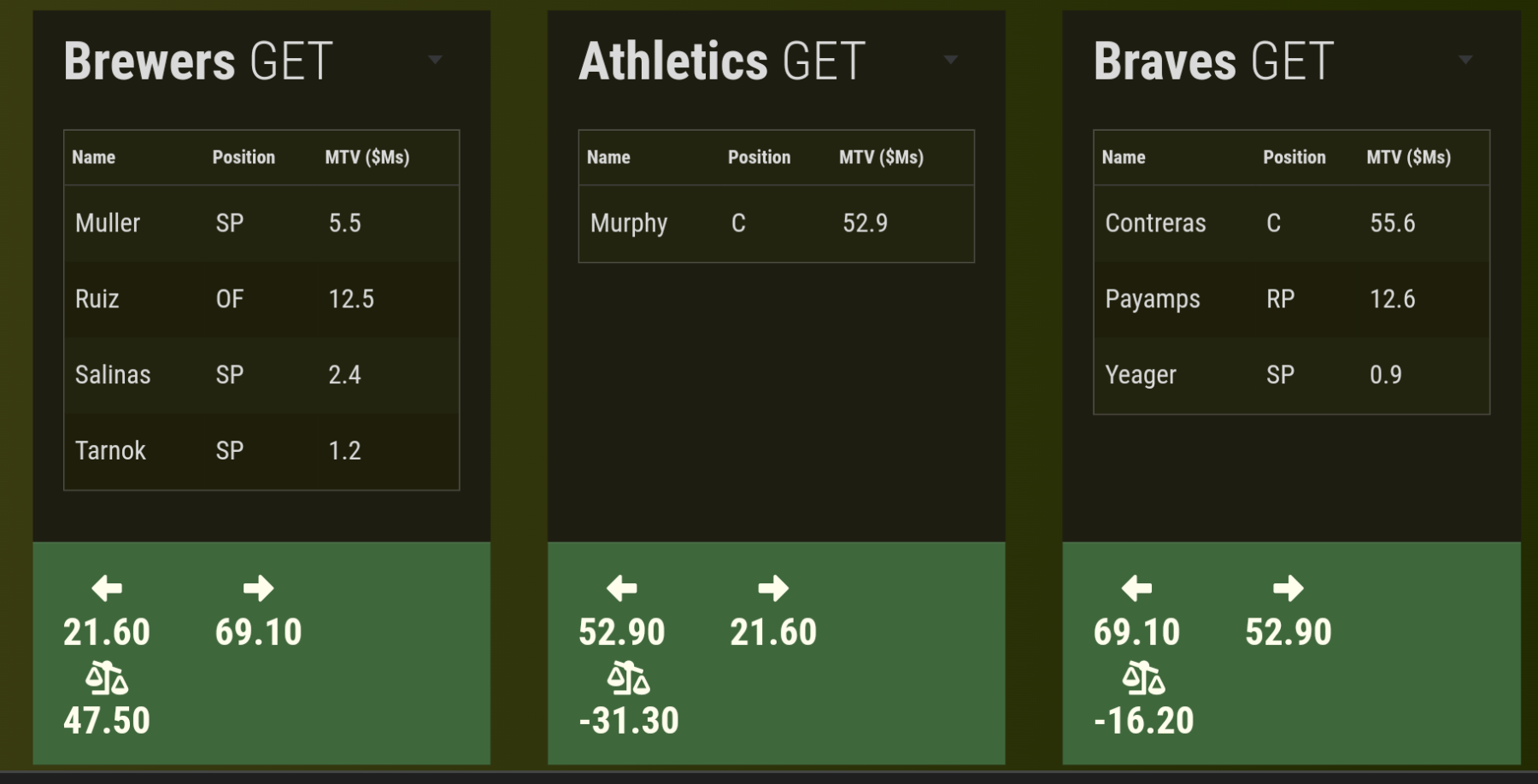

In retrospect, here is what the trade machine says about this trade now. The only part of it that I can't add is Manny Piña as he has been DFA'd by the A's (which had negative value originally). Brewers = Actual A's. A's = Actual Braves. Braves = Actual Brewers (as they should be). I think the only thing that is valid is the sum of the current gets as the gives came from different teams. I find it interesting that now the most valuable piece is Contreras...and Payamps (barely) has more value than Ruiz. Here is what values were at the time of the trade.

-

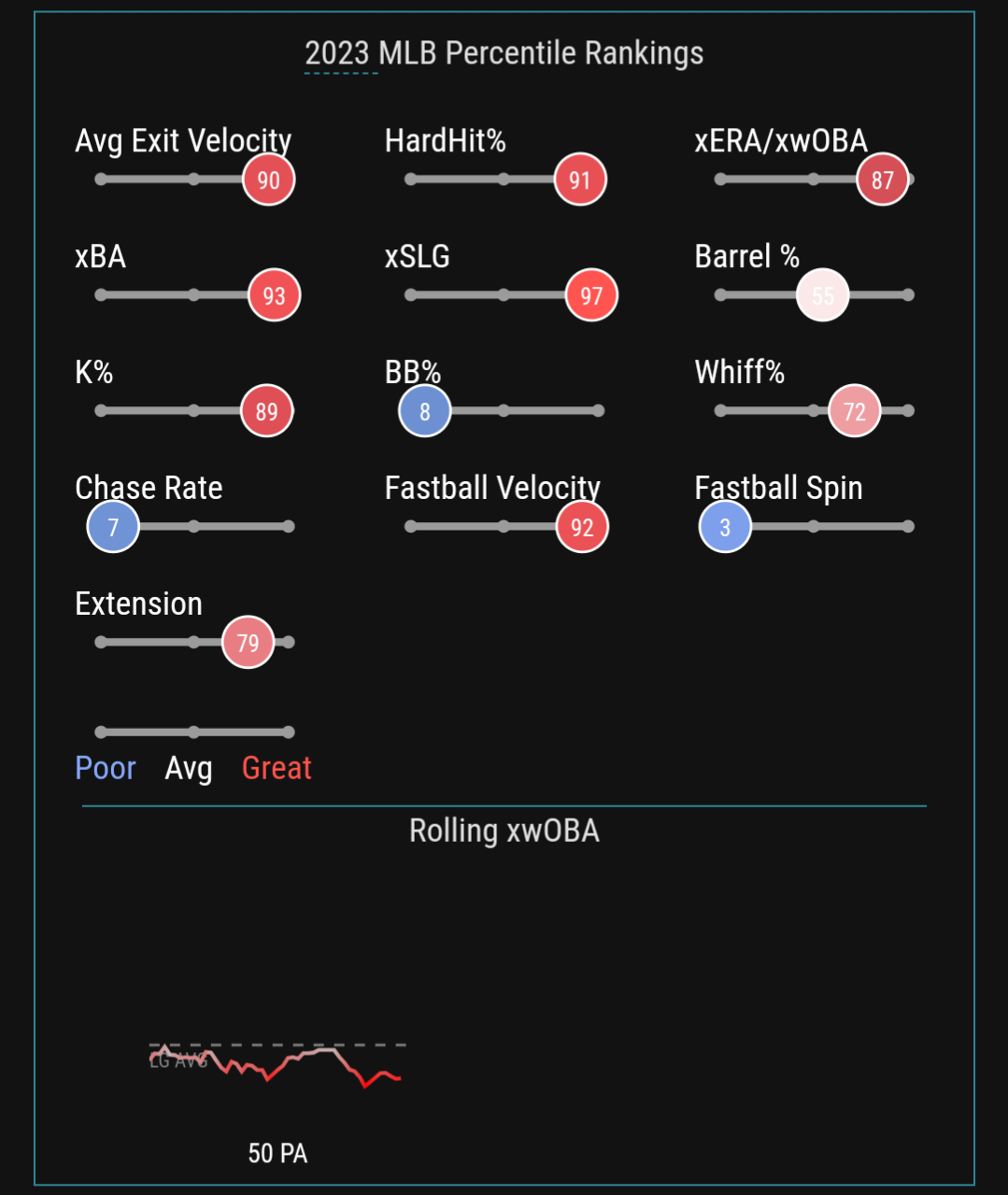

His xERA, FIP, and xFIP are all much more impressive. His statcast peripherals are below. It seems he walks over 5 batters an inning and his babip is also 0.400, which is not a good combo. Seeing that the hard hit percentage is in the 91st percentile, I wonder if his ERA would be better if he has the Brewers defense behind him. He's also only pitched 31 innings, so a lot can still change with that small of a sample. With that said, you can put me in the jury is still out on him camp. It seems the Brewers have cycled through a lot of these dime a dozen hard throwing high walk pitchers over the years, so maybe like you said, they know something more than what the peripherals I'm seeing are showing?

-

Just curious...shouldn't this article get banished to the trade rumors forum as I just don't see it ever coming to fruition? The Brewers organization is just too analytical.

-

I tried really hard to watch the World Cup. The lack of commercials is a definite positive. It was entertaining but I don't think I could watch it all the time. It's just a little bland for me (much like American Football where there is too much dead/commercial time). Soccer isn't a terrible sport by any means but as a fan of hockey, I also find offsides, the lack of substitutions, and the lack of shots on goal frustrating. The strategy between soccer and hockey is pretty much identical. I also used to hate on hockey and soccer until college. Having a roommate from Minnesota, I started getting into hockey. I can remember playing the video game with him for the first time where I got destroyed like 10-1 or something close to that. Then I started learning offsides and icing and some of the strategy and I was hooked (pun not intended). The commercials aren't terrible for NHL games either...14 10 and 6 minute marks of each period (assuming there isn't a break in the action or a power play). Additional, the offsides line is static, there are on-the-fly line changes where each shift is a minute or so, and way more shots on goal. At this point, I think I like soccer more than American Football. I would like to see soccer played with hockey rules. They could have boards to keep the ball in play and why not...checking. I think this may be indoor soccer (well without the checking) but I'm not sure.